As my Toastmasters journey continues, I have been reaping a lot of the benefits from being an active member. In my last post, I spoke about how taking a club officer role helped me in working on my leadership skills. In this post, I would like to share with you my experience from entering Club Level, Area Level and Division Level competitions. A few years ago, the idea of entering a speech contest would have terrified me since I was never comfortable speaking in front of people. Competing in a speech contest was a goal that I wanted to work towards but one that I felt was of my reach, however thanks to the confidence that I built in delivering speeches at my club and thanks to the warm support of my club members, I was able to finally reach this goal.

In a past post, I wrote about my experience in joining a Toastmasters Club. As I am writing this post, around a year and a half has passed since and there is a lot that I have gained from my involvement in Toastmasters. I have enjoyed it so much that I am now part of three clubs (yes, that’s a lot of time committed to Toastmasters). For those of you who have never heard about Toastmasters, you can refer to my previous post where I provide a general overview but to sum it up, it’s an organisation that helps its members develop their presentation and leadership skills.

What I would like to focus on in this post is the valuable experience that I have gained from taking the club officer role of president at one of my clubs. Every Toastmasters Club is managed by designated club officers who help in the running of the club by taking on core responsibilities that are essential for growing and maintaining a healthy club. These individuals are ordinary club members who put themselves forward at the start of an office term (more details can be found here) and are elected via the club’s officer election process.

While my first year at Toastmasters was focused on my presentation skills and on working on my speeches, my second year has been focused more on my club officer role. I have seen a lot of seasoned toastmasters who are just happy focusing on their speeches and avoid taking club officer roles due to several reasons (time commitment, additional responsibilities, etc.) but I think this is a big mistake as there is so much value from being a club officer. I believe that by taking on a club officer role, members can truly focus on harnessing their leadership skills. In this post I am summing up some of my key learnings:

A year ago I posted Top 5 Popular Stocks in Japan that Offer Yutai Gifts where I shared a popular list of yutai stocks. Given the interest received for that post, I created an updated list for 2020 that I would like to share with you. Some of my picks remain unchanged and it wouldn’t be interesting simply just re-introducing the same stocks so I will be doing something slightly different. Rather than ranking the “Top” stocks, I will introduce to you 5 stocks that pay out interesting yutai gifts.

There is a lot of material in Japanese, very often promoted by online brokers or other blogs and newsletters, but I couldn’t find a lot of content in English which is what led me to start this series of of posts.

Over the past months I have been preparing for the CMA (Certified Member Analyst of the Securities Analysts Association of Japan) exam and although this is a Japanese exam, they have test centres in London, Hong Kong and New York.Since I had some holidays booked to visit the US at the end of September, I opted to take the test in New York and so in this post I would like to share my experience.

Preparation

The exam is comprised of three sections: Accounting, Portfolio Management and Economics (you can read more about the structure of the exam here) and I had registered this time to take the Accounting portion since I had taken the remaining two parts in Japan. In preparing I made sure to go through past exam questions and practice questions. If you are enrolled for the exam you will have access to past exam papers from 2014 – from your MyPage Account. The below book by TAC is also widely used by candidates in their preparations; the book has the same past exam questions that you can access from your MyPage however the questions are neatly categorised based on topics and the answers are more thorough compared to what you will see from the institute papers.

Having seen numerous solved past papers OR Having seen and completed numerous past papers, I can say that the format has remained unchanged for years so if you have done your prep you shouldn’t have/experience any big surprises on test day.

Here is how the exam is structured:

Part 1 (concept checkers: 17 questions) In this section you will get conceptual questions on ALL topics and there will be no calculations involved. You will pretty much know straight away whether you know the answer, or you should at least be able to narrow down your answer to make an educated guess. Unlike parts 2,3,4 this part is difficult to prepare for given the breath of the topics.

Part 2,3 (calculation questions: 15 questions) The calculation questions which come up in these sections are pretty repetitive so this part should allow you to pick up a lot of points. Lease Accounting, Tax, Pension Accounting, Equity Valuations, Inventory Accounting are some of the most popular topics tested in this section.

Part 4 (financial statement analysis: 26 questions) In this section you are given a Balance Sheet and an Income Statement and you are asked to calculate a lot of financial ratios. Be sure to know how to calculate ROE (Du Pont Analysis), ROA, Efficiency Ratios, Safety Ratios, etc..

Please note that just like the other level 1 exams the entire Accounting Exam is also multiple choice based.

My Strategy

I did a lot of research to see how people tackled this exam and a lot of candidates recommended tackling the exam in the following order: Part 4, Part 2,3 and lastly Part 1. The format for Part 4 has remained unchanged in the last years so as long as you remember the formulas for the ratios and where to look for in the financial students for the relevant information, you should be able to get most of the points. When calculating ROE or any ratio that mixes income statements and balance sheet items, remember to take the average of the two fiscal periods for balance sheet items. For example, if you are calculating ROE (Net Income/Equity) for period T, make sure to calculate the Equity part in the denominator as Equity = (Equity_T-1 + Equity_T)/2.

Other than that, the rest is a lot of number crunching so being able to quickly compute ratios on your calculators should be very helpful. For the exam I chose to use the HP12C calculator which I also used throughout my CFA exams. I focused most of my energies on this part and aimed to get 100%.

Parts 2 and 3 have a bit more variety compared to part 4 but these questions should have popped up in past exams. I stepped in the exam room aiming to get around 70%+ in this section.

Finally, we come to Part 1 or I should call it the ‘wordy concept checker’ section which no one seems to like, myself included. Assuming I got most of my points from the remaining sections, I didn’t bother spending too much time here and aimed to get around 50%

Exam Day

Exam day was a perfectly sunny day, a day I would have preferred enjoying in Central Park rather than taking a Japanese financial analyst exam. The test centre was at the Silberman School of Social Work in East Harlem and my hotel was close to Time Square so I ended up getting the NYC metro from the Grand Central Terminal.

I had taken the exam in Tokyo and sitting it in Harlem it was a completely different experience compared to sitting the exam in Aoyama Gakuin or Waseda. New York was much less chaotic, and I was surprised to see that only 5 other candidates were taking the exam. Slight jet lag aside, I thought it was quite a fair exam and I stuck to my strategy of solving the numerical parts first and leaving the wordy Part 1 until last.

Although I have not yet received an official email from the institute, based on past years we can I expect results to come out in the first week of November. I felt very relieved after the exam and I did manage to go and spend some time in the sun enjoying Central Park.

Having lived in Japan for over 3 years now and having spent some time preparing for this exam, I thought it would be worthwhile writing about it. This is a Financial Analyst exam administered in Japanese twice a year by the Securities Analysts Association of Japan. To qualify for the charter, you will need to pass levels 1 and 2 and have 3 years of qualifying work experience. It goes without saying that if your Japanese is not near-native level you will find this exam quite tough.

Having met numerous professionals in the financial industry here

in Japan, I must say I was surprised by the number of people who have the

letters CMA on their business cards. In terms of prestige I would compare it to

the CFA, although the CFA is regarded more highly due in part to the perceived

difficulty with regards to the English language barrier that some Japanese

might face.

You will then have 3 years to pass all the required exams. Since

you can take the exams in both autumn and spring, that gives you 6 attempts to pass. If you don’t pass within

those allotted 6 attempts, you will need to pay the registration fee again.

Level 1 Topics

Level 1 is comprised of 3 topics: Economics (1.5 hours),

Accounting (1.5 hours) and Portfolio Management (3.0 hours). You can take ALL 3

exams on the same date or you can take the exams separately.

Economics: microeconomics (supply & demand curves),

macroeconomics (ISLM curves, Fiscal and Monetary Policy), FX theory (PPP, IRP).

Level 2 from what I have heard is a written exam (a bit like the

CFA level 3 constructive response) and I will cover this in more detail in a

future post.

Popular Learning Materials

As far as I have seen, TAC seems to have the monopoly when it

comes to learning materials for this exam. I would recommend purchasing the

below learning materials. The smaller books contain summaries of the topics and

the bigger books contain practice

questions that are based on past exam papers (the institute discloses past exam questions).

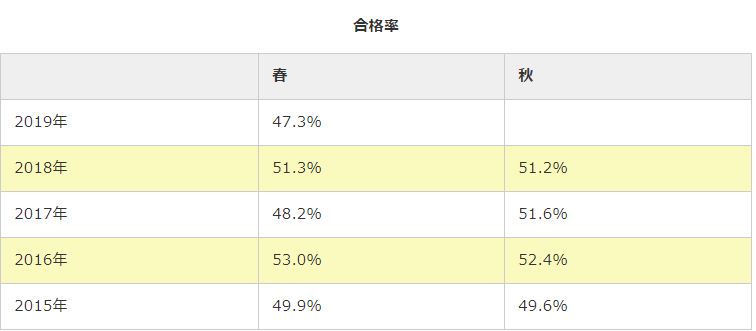

What are the Pass Rates?

These are the pass rates for the last 5 years, as you can see

roughly 50% of the candidates pass.

Final Thoughts

Having almost completed the level 1 exam, I must say that it is

not impossible to pass. This is especially true as unlike the CFA, you have a big

advantage that you can take the exams individually. You also have specific

types of questions that reoccur, so practising as many questions as possible

helps. A Japanese candidate would tend to spend 1-6 months preparing for the

exam depending on their background. I think the average (non-Japanese?)

candidate working in the financial sector should need 3-4 months to be

comfortable in his/her preparation. If you are considering taking the exam and

have any questions please do not hesitate to contact me!

So you’ve reached the final CFA exam. This is not something to be sniffed at so you should be proud of your achievements. You are almost there and I am hoping that this article will help you in your studies and will guide you towards the right direction, so please keep reading.

IPS is King

If you have done some research on the exam format or you have attempted past questions, I am sure that you have noticed that for the first time you are not faced with multiple choice questions and instead you will have what they call ‘constructed responses’. Yes, you will have to write sentences using pencil and paper rather than marking an answer sheet. An IPS which stands for Individual Policy Statement is a type of constructed response question that you will see in the morning session, needless to say you need to be scoring high on IPSs if you want to pass. Please note that the afternoon format is multiple choice.

If I was explaining what an IPS is to my grandmother, I would tell her that it’s an assessment of her current finances and set of financial goals. You need to picture yourself as a financial advisor, helping your client come to grips with his or her financial situation; this entails being aware of any assets that are held, sources of income or any expenses. Given your client’s financial situation you need to assess the below points:

Time horizon: what is your client’s time horizon? 10, 15 years? If we talk about inheritance this could extend to a longer period. Multi-generational time horizon is a buzz word you might want to take note of.

·Taxes: should there be any aspect that would cause a high tax expense, note this down and remember to emphasise tax efficient investing.

·Liquidity: liquidity is very important. After having assessed your client’s outflows, is their source of income sufficient enough to cover them? If there are a lot of foreseeable expenses and your client’s wealth is concentrated in illiquid real estate then liquidity could be a problem.

·Legal: you don’t tend to see this come up but always acknowledge that local laws apply and should there be applicable laws from multiple jurisdictions, mention that.

·Unique: you will easily notice this. This tends to be some unique situation that your client is in. For example, the majority of their wealth might come from their company or it could be their aversion towards sin stocks.Then you will need to assess your client’s ability and willingness to take risk. Willingness is more related to cognitive aspects, so make sure to pay attention to any traits or biases that the person could exhibit. Ability is more of an objective assessment. Does your client have a sufficiently large portfolio and a long-term time horizon? Then chances are he/she will be able to afford having a more aggressive portfolio to aim for higher returns in the long run. If instead your client is retired and their portfolio is their only source of income and they have numerous upcoming expenses, then chances are high that you should be conservative. You should recommend your client to invest in safe instruments that provide a steady, reliable stream of income.

OK so how do I nail an IPS question you might ask?

(1) Write concise and clear bullet points. When I was first tackling the questions I was making the mistake of writing long, convoluted sentences making it hard for the marker. The marker will have an answer key and will be ticking boxes to ensure that you covered the relevant points.

(2) Practise, practise, practise. You just need to get used to answering IPSs. A good thing about CFA Level 3 (unlike levels 1 and 2) you will have access to past morning exam papers, so make sure to attempt them and see what recommended responses the CFA Institute provides. When doing past papers though, be careful NOT to go too far back into the past as some of the questions will not be as relevant.

(3) If you have a study partner, try to mark each other’s papers. It might be helpful to have another person read your responses and give you some honest feedback as to whether you covered the main points. Sometimes when marking our own mocks we might give ourselves the benefit of the doubt whilst examiners might not.

(4) Passion. OK you might think that this might sound strange but try and think of yourself as a consultant or a financial advisor. Try and think of the people who pop-up in the question as if they were real clients, friends or family. After months or years of gruelling studies, you are the financial expert – what genuine advice would you give them so that they can reach their financial goals? I found approaching questions in this manner to be entertaining and helped concepts to stick in my mind.

Is CFA Level 2 harder than CFA Level 3?

This is a debate that I find very interesting. Some people pass level 2 and will tell you that you have cleared the hardest exam, others will tell you that level 3 is a real nightmare. I personally think that if you are the technical and mechanical type, you will find level 2 a fair exam. You should not approach level 3 with the same mind-set that you had for level 2, I certainly did and got punished for it. This might sound abstract but for level 3 you need to see the big picture. Level 3 isn’t about how quickly you can value swaps or calculate free cash flows, it’s about being able to understand your client’s situation and applying sound judgement in addition to technical knowledge. Level 3 takes for granted that you have understood the core concepts and requires you to put them into practise in the field of portfolio management. For this reason if you have started preparing for level 3, I would personally recommend just skimming through the whole curriculum and getting a general idea, then going into the nitty gritty details.

Although the CFA exam isn’t a number crunching exam, you will come across numerous questions that require the use of a calculator. Your two weapons of choice are the Texas Instrument BA II Plus and the Hewlett Packard 12C. Before buying your calculator, make sure to read the CFA Exam Calculator Policy that can be found here.

Also, if you are undecided between the two makes and you

would like to try them, both brands have apps that you can go to your phone’s App

Store and download. In terms of functionality the apps are identical to the

physical calculators.

The main purpose of this article is to make you aware of the

type of operations that you should know how to do via your calculator prior to

attempting to sit the exam.

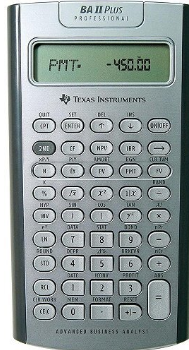

I will be using the BA II Plus for my explanations and

examples (I will make a separate tutorial for Hewlett Packard lovers)

(1) Present Value/Future Value [Priority = High]

What is it? Other than being able to quickly perform basic

arithmetic operations on your calculator, I think this is probably one of the

most important things you will need to be able to do. You will be given the

amount of money in the bank account (PV), the prevailing interest rate and the

period of time over which the interest will compound and from this you will

need to compute the future value. You can be given any of the inputs and solve

for the missing one.

If you have started with the basics and the concept of Time Value of Money is obscure to you, you might find this article helpful.

This is also applicable to fixed income where you have the

market price of the bond, coupon payments and coupon payments frequency and you

will need to compute the IRR of the bond. You can easily compute the present

value of annuities or lease payments in Financial Reporting. Yes, simple Time

Value of Money calculations are ubiquitous on the CFA exams so let’s get started.

Examples:

Q. A bond is trading at $102, it pays 5% coupon per annum

and matures in 2 years. What is the bond’s yield?

A. Mathematically this is what you would see if you applied the formula for calculating the yield:

If we look at the above formula for calculating the present value of a bond we can see that we are given everything except the y (for those who have studied corporate finance you can see that this is comparable to getting the IRR of a project), for the face value we can assume that it pays $100 at maturity. This gives us the below formula:

We will be using the grey buttons of our BA II Plus in the

red box.

After ensuring that you have cleared the memory (2ND function + CE|C)

Please key in the following:

2 N button

(you will see N = 2)

-102 PV (you

will see PV = -102, make sure to put the negative sign here)

5 PMT (you

will see PMT = 5, this was calculated as coupon rate * par or 5% * 100 = 5)

100 FV (you

will see FV = 100)

Now that you

have keyed in all the data, press the “CPT” key on the top left corner and

press “I/Y”. If you keyed in everything correctly you will see that your yield

is around 3.94%. If you press CPT and any of the inputs that you keyed in, you

can verify what data has been entered. For example CPT PMT will still show you

5.

This was a very brief example but try playing around with

the numbers, try changing the assumptions; for example you could easily verify

that the price of the bond falls as you increase the Yield (I/Y) by gradually

increasing the yield.

My example assumed that the coupon payment was 5% annual but

if you were told instead that the coupon was 2.5% semi-annual, remember to also

multiple the N * 2. At first, if you are not sure draw a diagram of all the

future cash flows.

(2) NPV/IRR [Priority = Medium]

What is it? Although there is an overlap with the

previous topic, I thought this part deserved its own section. With regards to overlap

I mean that we are still asking the calculator to compute present values, summing

them or solving for IRRs. For some examples you can use the PMT button as shown

above to get an answer to NPV and IRR questions. However, the limitation is

that PMT only takes the same cash flows, i.e. if you are looking for the

present value of something that pays $100 over 10 years at a fixed rate, let’s

say 5% cost of capital, then you can just key in 10 N with 5 I/Y followed by 100

PMT and 0 FV then pressing CPT PV to get your answer of -$772.17. What about a question to calculate the present

value of a project that requires an investment of -$1000 at initiation or year 0,

then pays $500 in year 1, $300 in year 2 and $400 in year 3. Your cost of

capital is 3%. This is where you cannot

use PMT and you need to key in the cash flows for discounting.

Examples: I will

use the example that I just introduced. Again this is a simplified example to

illustrate the steps and you should definitely expect harder questions.

The below formula will yield the NPV for this project:

Plugging in the numbers we get:

Now let’s obtain this number on the calculator.

Please key in the following:

CF (this button just next to the yellow 2nd key),

you should see CF(0) = 0, now just to be sure that we don’t have any data from

previous exercises, please clear the memory by pressing 2ND function

+ CE|C. Once you have done this you can press the up and down arrow keys that

are found on the top right next to the ON/OFF button to see what data is stored.

You should see CF(0) = 0, C01 = 0, F01 =0. We are ready to start:

CF(0) =

-1000 ENTER, you will see CF(0) = -1000. Press the down arrow to key in the

next cash flow.

C01 = 500 ENTER

you will see C01 = 500. If you press the down arrow key you will see F01 = 1. This

indicates the frequency of the cash flows. For example if you want the same

cash flow of 500 being paid 3 times from years 1 to 3 then you can enter 3. In

our case we have only one payment so we will keep the default value of 1 and

press the down arrow again.

Now you will

see C02 and you will be able to enter the second cash flow of 300. Repeat this for

the final cash flow of 400 and once you have entered all the cash flow data we

can compute the NPV.

You should see

C03 = 400 on your calculator. Now press the NPV button and you will see I = 0

on your calculator. Key in 5 and then press ENTER (important to note that 5

will be 5% so do not enter 0.05 otherwise you will enter 0.05%) now press the

down arrow and you will see NPV = 0. Press the CPT key on the top left and you

will see the NPV result of 93.83 and we are done. If you want to amend your

rate you can press the up arrow which will display the “I”, enter a new rate

and again press the down arrow and press CPT to calculate the NPV on the new

updated rate.

(3) Storing Results [Priority = High]

What is it? You can use the STO and RCL keys to store

calculation results and quickly recall them for future use. Before I was aware

of this feature I used to write down any interim calculation results on paper,

then I used to key in those results in my calculator to perform calculations. This

had some drawbacks as it was time consuming and prone to careless errors, not

to mention the loss of accuracy due to rounding.

Example: for

example let’s say 105.723 is your answer and you want to store this value for

future use, press STO and then any number on your number key that you want to

use to store this value. Let’s say I want the number “7” to store this value

press the key order STO 7. Now try entering any number or clearing your work

with CE|C. Now you can recall the previous number that we stored in memory by

pressing RCL and “7”, magically 105.723 will appear on your calculator.

Yutai Gifts 株主優待 (Kabunushi Yutai) are perks that companies give to their shareholders as a form of gratitude for owning their stocks. These gifts are often tied to the product or service that the company provides. A lot of retail investors find Yutai investing appealing and there are numerous websites in Japanese that summarise and rank these Yutai offerings. I have done my own bit of research and I have come across quite a few companies that provide competitive rewards. Over the months I have created my own list of popular Yutai stocks that I would like to share with you.

How do I receive my Yutai Gift?

Before we get started with our top 5 list, you might be asking what is required to be eligible to receive these gifts.

You will need a brokerage account in order to purchase the stocks. For guidance in opening up a brokerage account in Japan, please refer to this article.

Purchase the stock and hold it until the relevant ex-right date (the date on which you are eligible for the gift if you are the shareholder).

You will receive your Yutai Gift via post (most companies have a detailed description on their website regarding the Yutai Gift timings so you will be able to check online the exact dates of when you can expect to receive your rewards.

Now, let’s get started. All share prices are based on closing prices of 16th May 2019.

Company Profile: Skylark Group runs numerous family restaurant chains in Japan. Gusto and Jonathan’s were the two restaurants that I was aware of but their brand portfolio seems quite extensive and includes a wide range of cuisines. You can find a list here.

Gift: Coupons that can be used across their restaurants. Every 6 months you will receive 3,000 JPY worth of coupons so that’s 6,000 JPY per year just in coupons which isn’t that bad (these coupons are relatively easy to sell online or at ticket shops like Daikokuya.

Company Profile: McDonald’s needs no introduction; their burgers are widely consumed around the world and Japan is no exception.

Gift: You get the below booklet which has 6 sheets. Each sheet has 3 coupons which can be exchanged for 1 burger, 1 side and 1 drink or dessert of your choice. I have seen people assigning different values to this coupon. Some people came up with their valuations by picking the most expensive items on the menu that they can order, which brings the monetary value of a booklet close to 7000 – 8000 JPY. I have seen more fair estimates which value this coupon at around 5000 JPY.

Minimum Shares Required: 100 shares

Investment Amount: 4880 * 100 = 480,000 JPY

(3) ANA Holdings (9202) / JAL (9201) ( (I put both airline companies together as what they have to offer is pretty similar in my opinion).

Company Profile: JAL and ANA are the two biggest domestic airlines in Japan and are with well established internationally.

Gift: 50% off domestic flights. Considering domestic flights can range from 20,000-50,000 JPY, you are looking to save 10,000 – 25,000 JPY on your travel fare. Similarly to other Yutai Gift tickets you will be able to easily sell them online.

Minimum Shares Required: 100 shares (to note that the number of free tickets increases as the number of shares increase). For JAL this website (in Japanese) has a good summary of the benefits, there are also added bonuses such as additional coupons for holding the stock for 3 consecutive years.

Company Profile: Headquartered in Urayasu, Oriental Land runs Disney Land and DisneySea, two very popular theme parks in Chiba. In addition to its theme park business, the company also manages a number of hotels including the Disney Ambassador Hotel.

Gift: 1 free entry pass for either Disney Land or DisneySea (entry price for adults is 7,400 JPY). If you are a fan of Disney and their theme parks I could definitely see the appeal for this gift. Alternatively the coupon can also be easily sold online as there is huge demand for it.

Company Profile: Aeon runs a large chain of supermarkets across Japan and Asia. If you hold their shares you will be sent their “Owner’s Card”. This will entitle you to claiming 3% cash back on your purchases made in cash or via Aeon credit cards (please note that purchases made with non-approved credit cards will not be counted) at their stores. If you regularly do your shopping at Aeon the cash back becomes quite appealing. Similarly to other Yutai gifts, you will entitled to cash back every 6 months. For example, let’s say that over the past 6 months you spent 500,000 JPY at Aeon, your cash back amount will be 500,000 * 0.03 = 15,000 JPY. Considering the stock trades at around 2000 JPY, that’s 15,000/200,000 = 7.5% yield and we are not even including dividends.

Gift: 3% cashback card.

Minimum Shares Required: 100

Investment Amount: 1989 * 100 = 198,900 JPY

What are your top picks? Have you come across any good stocks with Yutai gifts? Please post your top picks in the comment section. Thank you for reading.

The Dividend Discount Model, also known as

the Gordon Growth Model is a formula that allows us to calculate the intrinsic

value of a stock. The model assumes that the fair value of a stock is the present

value of all future dividends that the company pays to its shareholders. These

dividends are discounted to present value by using the required rate of return

for the stock.

We firstly assume a model where the

dividend amounts are fixed.

As

we obtain

This result is what we call a perpetuity (an annuity that pays fixed cash flows at constant intervals until infinity). The model assumes that all company dividends are paid out therefore there is no growth in the company’s dividends. Very rarely, companies pay out all their earnings in dividends, instead a proportion of earnings are retained internally to help grow the company in the future. By adding this assumption we introduce the company’s “sustainable growth rate”. This is the constant rate at which we assume that the company and therefore the dividends will grow in the future.

As

We obtain (a growing perpetuity):

Limitations

The model isn’t applicable to

companies that currently do not pay dividends.

Dividend amounts may fluctuate over

the course of the years, so it might not make sense to assume that they are

constant. In such cases we need to look at more complicated models like a two-stage

dividend growth model.

The model requires precise estimation

as the stock price is very sensitive to the assumptions that we place for the

growth rate (g) and the required rate of return (r).

Advantages

Well known and relatively

simple to use.

Applicable to well established

companies that have a long track record of paying out dividends.

Worked Examples

Question

1

Company A pays $80 in dividends and is

expected to pay the same dividend amount forever. Investors require a 10% rate

of return for this stock. What is the intrinsic value of the stock?

‘Answer: 80/0.10 = $800

Question

2

Company B pays $25 in dividends and is

expected to pay the same dividend amount forever. Investors require a 5% rate

of return for this stock. What is the intrinsic value of the stock?

‘Answer: 25/0.05 = $500

Question

3

Company C is expected to pay a dividend of $35

next year. The company’s sustainable growth rate is 5% this growth rate is

expected to be constant. Investors require a 7% rate of return for this stock. What

is the intrinsic value of the stock?

‘Answer: 35/(0.07-0.05) = $1750

Question

4

Company C is expected to pay a dividend of $2

next year. The company’s sustainable growth rate is 2% this growth rate is

expected to be constant. Investors require a 12% rate of return for this stock.

What is the intrinsic value of the stock?

‘Answer: 2/(0.12-0.02) = $20

Feel free to post any questions you may have. Happy Studying!

So, you are seriously considering taking the CFA exam and you might be looking for some information online, if so, congratulations you have come to the right place. I sat and passed the exam back in 2011 and I would be happy to share my advice here. Luckily, not much has changed since then with regards to the test format and the content so I believe that what I cover in this post is still valid for candidates preparing for the exam today.

Topics Covered

The CFA Institute provides here a detailed overview of topics which are covered in each level. Not all topics are weighted equally so successful candidates are good at identifying core topics and questions and are able to focus on these areas in their preparation. The learning focus according to the CFA Institute is “Knowledge and Comprehension” rather than “Application and Analysis” which will be tested in Level 2. In my opinion, Level 1 is all about the candidate gaining a general knowledge of all topics whilst grasping the foundation of investment analysis concepts which he/she will use later on in performing investment analysis.

Exam Format and Exam Strategy

The exam consists of a morning and afternoon part, each containing 120 multiple choice questions (to note that there is no negative marking so do not leave any questions blank). You will have 3 hours to complete the questions so you will be under a lot of time pressure. It’s important to avoid spending too much time on any single question so if you are not sure about a question, mark it and come back to it later. Aim not to spend more than 90 seconds on a single question, there won’t be long calculations involved so if you have a good mastery of the topic you should be able to come up with an answer relatively quickly. When I took the exam I aimed to finish the exam in an hour so I had the last 20-30 minutes to review my answers. As you take mock exams you will develop your own test taking technique but the key point that I want to get across is that pacing yourself is as important as your knowledge of the curriculum.

Study Resources

The moment you register for the CFA Institute you will get access to the Institute Curriculum which will be shared to you as an E-Book. I also recommend ordering the hard copies of the Institute books which will be sent to you via post. The whole curriculum consists of 6 thick volumes that will take a lot of space up and will be a perfect substitute-friend for the upcoming 6 months or so. The question that a lot of candidates ask themselves now is whether the Institute materials are enough or if they require some additional source of help in the form of study notes or video lectures. Schweser is a very popular choice amongst candidates. Others might also opt to take classes via other training providers. So, are training providers worth the additional cost? It really depends on the candidate’s background and circumstances in my opinion. If a person already has a good finance background and has time to commit in reading the curriculum I don’t think he/she needs to rely on training providers. If instead time is a constraint or finance is a new subject then possibly the additional help will provide to be valuable and worth it. Overall I think training providers have done a very good job in analysing the exam, identifying the key topics and ensuring that their students have a high chance of passing. My experience with them has been positive.

The Calculator is your Friend

There are only two types of calculators that you will be able to take into the exam with you – read the official Calculator Policy here – Texas Instruments BA II Plus and Hewlett Packard 12C. If you have registered for the exam and you are in the early stages of your preparation my advice is to start getting familiar with the calculator as soon as possible. There are a lot of questions on the exam where you will need it and you will be able to quickly score valuable points. Some examples of where your calculator will come in handy are: Present Value/Future Value, Bond Calculations, NPVs (maybe some Statistics functions and Annuity calculations).

Last Words of Advice

Remember to do the end of chapter questions in the official CFA books. All questions are of high quality and are very likely to be tested on exam day.

Do not have a heavy lunch in between the morning and afternoon exam.

Remember your exam ticket and passport on exam day otherwise you will not be able to sit the exam that day.

Think of your study as a marathon not as a sprint, towards the final week of the exam do some light revision and preserve your energies for exam day.

Get yourself a nice study group to have people who you can share your joys and pain with.

Thank you for reading and I hope you look forward to future posts.