Throughout your studies of fixed income, very often you will have come across the concept of Duration. So why is it so important? Duration measures the sensitivity of your bond to changes in interest rate. Let’s say interest rates drop 1%, by using duration you can get a rough approximation of how much your bond price changes.

Bond Price and Interest Rates

Before we get started with Duration, let’s talk about bond prices and interest rates. You might have heard the expression that bond prices and interest rates are negatively related. Interest rates go down and your bond price rises, interest rates rise and your bond price drops. This is because the value of your bond is the summation of the present value of all future cash flows, so the higher your discount rate (interest rate) the lower the price of your bond.

Let’s assume that we have a bond that pays a 5% yearly coupon with a face value of 100, prevailing yields are 6% across all tenures. For simplicity, I am assuming that we have a flat yield curve with interest rates constant across all tenures.

| Assumptions | ||||

| Coupon | 0.05 | |||

| Face Value | 100 | |||

| Yield | 0.06 | |||

| Years | CFs | CFs PV | ||

| Year 1 | 1 | 5 | 4.7170 | |

| Year 2 | 2 | 5 | 4.4500 | |

| Year 3 | 3 | 5 | 4.1981 | |

| Year 4 | 4 | 5 | 3.9605 | |

| Year 5 | 5 | 105 | 78.4621 | |

| Bond Price | 95.78764 |

As the the coupon rate of 5% is lower than the prevailing 6% rates, the bond is trading under par. Given the above assumptions we will calculate two key duration measures, the Macaulay Duration and the Modified Duration.

The formula for Macaulay Duration is as follows:

Where

The formula for the Modified Duration is as follows:

Applying the formula we obtain 4.32 for the Modified Duration.

Now that we have the Modified Duration for this bond we can evaluate its sensitivity to changes in interest rates. The expected change in the bond price can be approximated by Modified Duration * Change in Rate * Bond Price. Looking at our example, if we assume that interest rates drop from 6% to 4%, then -4.32 * -0.02 * 95.79 = 8.27 is our estimated change in bond price and in reality we saw that the bond did rise by 8.66 so we can see that our approximation was quite accurate.

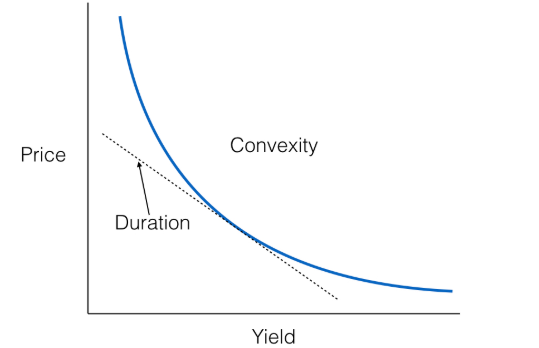

Duration however is only accurate for small changes in interest rates as it is only a linear approximation; we can see from the below graph that the relationship between interest rates and price is convex.

If Duration is the first order derivative between price and interest rates, we can better approximate the actual change in price by adding a second order term in the form of Convexity. I will be covering this in future posts in addition to other Duration measures such as Key Rate Duration and Effective Duration.