If you are reading this post, chances are you’ve passed the

Level 1 exam. If that’s the case, congratulations, that’s a great achievement!

Give yourself a pat on the back before you start worrying about how to tackle

level 2.

In the Level 2 exam you are tested in the form of 20 case studies or item sets (10 in the morning and 10 in the afternoon). Each item set has 6 questions so that’s a total of 120 questions in 6 hours. The topic weights can be found here.

Compared to the level 1 exam, level 2 goes into much more

detail in terms of testing concepts. If the theme of the questions in level 1

were “Do you know it?” level 2 instead asks “Can you apply it?”. A lot of candidates

end up failing this exam as they find the number of formulas overwhelming and

intimidating. In this post I have summarised some advice that I received when

preparing for the exam, advice that I hope helps you pass the exam.

(1) Don’t try to

memorise the formulas but try to see the big picture.

I’ve seen so many candidates trying to just blindly memorise

and apply formulas, losing sight of the big picture. This is dangerous in my

opinion. If you are the type who does well in memorising and applying formulas,

then I’m not here to dispute your exam technique. If you have tried doing a few

mocks and have been constantly scoring +60% then by all means please stick to

your way. What I am trying to say is that from my experience, I struggled when

I attempted to memorise all the formulas and when I applied a more intuitive

approach in solving questions that worked for me. This might sound a bit

abstract so let me give you an example.

Let’s say you are looking at Economics where you might be asked to adjust the exchange rate using PPP (Purchasing Power Parity). In our example we will use Japan and the US, the exchange rate is USD/JPY = 110 JPY and the inflation rate in the respective countries is 1% and 2%. The essence of PPP is that whether you buy goods in Japan or the US it shouldn’t make a difference. If goods are becoming more expensive in the US compared to Japan, i.e. higher inflation, this will be reflected in the expected exchange rate where Japan is the domestic currency and the inflation is for a 1 year horizon.

OK, you might ask what’s so hard about applying such a seemingly

innocent formula. To start with, I have seen a lot of candidates spending a lot

of time in trying to figure out how the exchange rate is quoted, which currency

is domestic and which one is foreign (others used quoted and base); add the

pressure under exam conditions and you are prone to make mistakes. The way I

used to approach this question was to tell myself: OK, inflation rates are

higher in the US and that means that their currency will have to weaken against

the Yen. I would apply the formula and check my result. I can see that indeed

108.92 < 110. At first 1 USD could get you 110 JPY, now it can get you only

108.92 JPY. Indeed the Yen has strengthened (or the Dollar has weakened).

Should I have accidentally flipped the numerator and the denominator, this

check would have allowed me to detect my mistake. This was just a simple

example but this way of thinking can be applied to many other questions on the

CFA exam. There are a lot of red herrings on the exams so being able to spot

and avoid them is a key factor in your exam success.

(2) Tips for Level 1

are still valid.

What I covered in my CFA level 1 post is also applicable to Level 2. Pay attention to the exam weightings in your preparation to ensure that you are scoring well in heavy topics like accounting and equity. Decide whether you want to pay a training provider or whether you have the time and discipline to self-study; this is definitely something you want to consider if your job is taking up a lot of revision time. The competition in Level 2 is fierce and chances are slim that you will pass with just 1-2 months of cramming. This is an exam where candidates who put in 200+ hours of studying end up failing.

(3) Don’t read the whole item set before

attempting the questions

When I first

started tackling exam questions I used to read the whole case study before

moving on to the questions. My mind was bombarded with information and the

questions were very detailed so I found myself going back to the item set and

looking for key piece of information, then going back to the questions, going

back and forth. Needless to say, I was struggling with time. It was only throughout

my revision that I realised the obvious; item sets are very often divided into

paragraphs and there tends to be a one to one map between paragraphs and

corresponding questions. Just to be clear, if there are 3 paragraphs and 3

questions, paragraph 1 will have the information that you need for question 1, paragraph

2 will have the information for question 2 and so on. My advice is to first

read the questions and then start reading the item set; when you are reading the

item set, if you think you have identified some information that will help you

solve any of the questions, then solve the questions before moving on. This

approach also helped me from a mental perspective as when I was done reading

the item set I wouldn’t be going back to 6 blank questions.

(4) Find a topic

where you can differentiate yourself from other candidates

In order to pass the CFA exam you will need to achieve what they call a minimum passing score; the CFA institute uses the Angoff Standard Setting Method in determining this. If you are getting the bulk of your points from easy questions, chances are that other people sitting the exam will be getting those as well. If overall the exam was an easy exam the pass rate will be set higher and therefore even if you do average or just slightly below average, chances are that you will fail the exam. You obviously need to get points in the easy questions but you also need to score in questions where other candidates struggle to get an edge over them. In my case, for level 2, derivatives was the area that helped me. A lot of candidates around me had given up hope on derivatives as they found a lot of the questions challenging. I persevered and I was rewarded on exam day.

I hope you found this advice useful and don’t forget to

leave your comments. Good luck with your preparation and with your CFA journey!

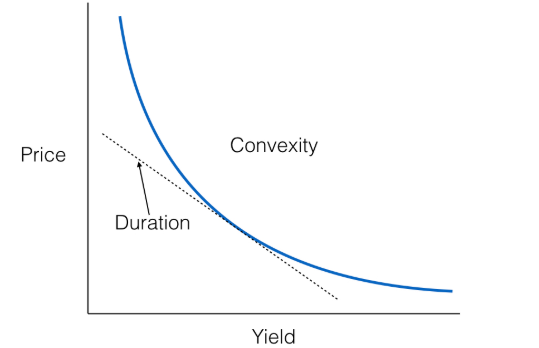

is the price of the bond,

is the price of the bond,  is the yield to maturity and

is the yield to maturity and  is the year. Applying the formula in our example we get that the Macaulay Duration is 4.53 years. We can interpret this figure as the average number of years that it would take for the bond to repay the initial investment.

is the year. Applying the formula in our example we get that the Macaulay Duration is 4.53 years. We can interpret this figure as the average number of years that it would take for the bond to repay the initial investment.