So, you are interested in alternative investments and you are seriously considering taking the CAIA exam? I passed the level 1 and level 2 exams a few years ago and I would like to provide you with some genuine pieces of advice that I hope you will find useful.

For those who have not come across this qualification, CAIA stands for Chartered Alternative Investment Analyst and the whole exam goes into a lot of depth in testing candidates about alternative investments. If you are interested in learning about common hedge fund strategies, going deeper into commodities and real assets, I think you will enjoy studying for the exam. I certainly did.

What is tested and how are topics weighted?

| CAIA Level 1 Topics | Exam weight |

| Professional Standards and Ethics | 15% – 20% |

| Introduction to Alternative Investments | 20% – 25% |

| Real Assets (Including Commodities) | 10% – 20% |

| Hedge Funds | 10% – 20% |

| Private Equity | 5% – 10% |

| Structured Products | 10% – 15% |

| Risk Management and Portfolio Management | 5% – 10% |

Exam Format

If you want to become a CAIA Charterholder you will have to complete two exams in addition to meeting other requirements, such as four years of work experience or a bachelor’s degree with one year of work experience. For level 1 you will have 4 hours to complete 200 multiple choice questions (you can choose to take a 30 minute break which I strongly recommend you do). You will also have a total of 4 hours for level 2, however this time in addition to 100 multiple choice questions you will have a section on constructed responses. A plus if you have already completed the CFA exam is that the ethics portion tests you on the CFA Standards of Conduct, so for this section you have killed two birds with one stone.

Unlike the CFA exam, the CAIA exam is computer based; so if you are like me and you enjoy marking answer sheets with your HP pencil you will be disappointed. You will be spending hours staring in front of a computer screen so if you decide to take the exam make sure to take online mock exams so you get used to starting at a screen for a long period of time.

Exam Windows

An advantage of the exam being computer based is that there is some flexibility with regards to the dates on which you can sit the test. The exam windows for 2019 are:

- Level 1: September 2 – 13

- Level 2: September 16-27

How to prepare for the exam?

The CAIA institute provides core textbooks for each level (materials can be found here). The Chapter Head for CAIA is Keith Black and his research is very well respected in the field.

It goes without saying that there are a few training providers out there who sell their study notes. I have had a look at the Schweser ones and similarly to the CFA study notes they are well written and the information is summarised well. However, in my case, going through the curriculum and doing a few mocks was more than enough.

Overall I’d say that if you have some foundations in finance, 100 – 200 hours for level 1 and 200 to 250 hours for level 2, this should allow you to pass the exam. Don’t be fooled by the pass rates, it’s definitely not an exam that you want to underestimate, especially level 2.

How to tackle item sets in level 2

If you have been used to answering multiple choice questions, the idea of typing your responses for item set questions might be intimidating. From my experience the markers will mainly focus on content and you shouldn’t get marked down for your style although clear and well structured responses will be appreciated. My advice is to provide short clear and concise bullet point answers.

General thoughts regarding the exam

Ok, if you have read this far you might be asking yourself if overall the exam is worth taking. The short answer in my opinion is “Yes” but again this will depend on your situation and your career goals. If you think this qualification will help you get hired straight away in a VC fund then you will need to reassess your expectations. The alternative investments industry is extremely competitive and you will need more than a qualification to differentiate yourself from the competition. I think the exam has the following two benefits:

- The curriculum is very well structured and provides a good overview of alternative investments. Upon completing it I felt like I knew a bit of everything regarding alternative investments; as a professional working in the financial sector it definitely helps having awareness of a wide range of asset classes.

- The network. I attended several events and I have had the pleasure of meeting William (Bill) J. Kelly, CEO of the CAIA Association. I had a very positive experience talking to him and I could feel his drive and passion in expanding this association globally. The events that I attended were in Tokyo and although the society is still relatively small compared to other capital cities, I am confident that it will keep growing in popularity. A lot of the charterholders here in Japan are quite senior people who have pursued the exam with the sole purpose of expanding their knowledge, so if learning is a key priority in life you will meet a lot of like minded people.

In future posts I intend to cover some topics that I especially enjoyed studying when prepping for the exams, so hopefully you will be able to use the content for your preparation. Thanks for reading and good luck with your studies.

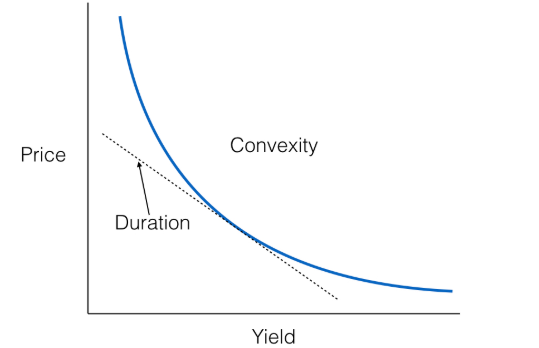

is the price of the bond,

is the price of the bond,  is the yield to maturity and

is the yield to maturity and  is the year. Applying the formula in our example we get that the Macaulay Duration is 4.53 years. We can interpret this figure as the average number of years that it would take for the bond to repay the initial investment.

is the year. Applying the formula in our example we get that the Macaulay Duration is 4.53 years. We can interpret this figure as the average number of years that it would take for the bond to repay the initial investment.